Crunching the Numbers: Your Guide to Term Insurance Calculators

Loan in

60 Minutes

Introduction

Life is full of uncertainties, and it's essential to plan for the financial well-being of your loved ones in case something unforeseen happens. Term insurance is a straightforward and cost-effective way to provide financial security to your family. To determine the right amount of coverage, you can turn to a term insurance calculator. In this blog, we'll explore what a term insurance calculator is and how to use it effectively.

What is Term Insurance?

Term insurance is a type of life insurance that provides coverage for a specified period, typically 10, 20, or 30 years. If the insured person passes away during the policy term, the insurer pays a death benefit to the beneficiaries. It's designed to provide financial support to your loved ones, ensuring their well-being if you're no longer around to provide for them.

What is a Term Insurance Calculator?

A term insurance calculator is an online tool provided by insurance companies and financial websites to help you determine the ideal amount of coverage you need. It's a user-friendly and efficient way to calculate the right coverage amount by taking into account various factors like your age, income, expenses, and financial goals. The goal is to ensure that your family has enough financial support to maintain their lifestyle and cover expenses if you're not there.

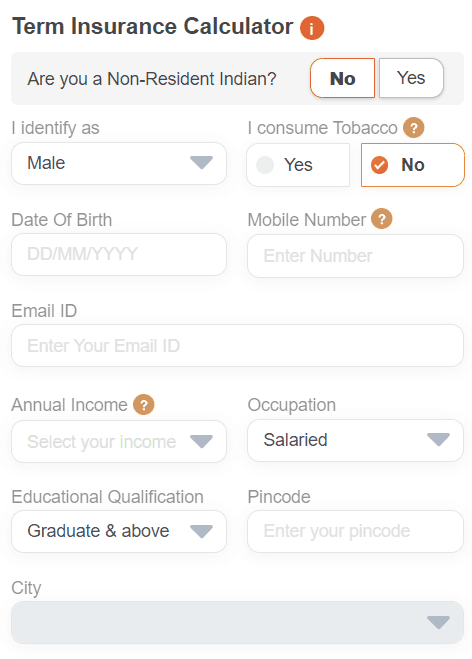

Components of a Term Insurance Calculator

A term insurance calculator typically comprises various key elements and inputs to help you determine the appropriate coverage amount for your specific financial situation. Here are the essential elements found in a term insurance calculator:

Basic Personal Information:

- Age: Your current age is a significant factor in determining the cost of insurance, as premiums tend to increase with age.

- Gender: Insurance companies often consider gender when calculating premiums, as men and women may have different life expectancies and risk factors.

Financial Information:

- Annual Income: Your yearly earnings are crucial because they provide an understanding of the financial support your family would require if you were no longer around.

- Existing Savings and Investments: This includes any savings accounts, investments, or assets that your family could access in the event of your passing.

Living Expenses:

- Current Monthly or Annual Expenses: These expenses encompass your day-to-day living costs, such as mortgage or rent, utilities, groceries, and other regular expenditures.

Outstanding Debts:

- Loans and Mortgages: Outstanding debts like home loans, car loans, and credit card balances should be considered since your family may need to settle these obligations if you pass away.

Number of Dependents:

- The calculator will ask you to specify the number of dependents who rely on your financial support, such as children, spouses, or aging parents.

Coverage Period:

- Choose the term length for your term insurance policy. Common term durations include 10, 20, or 30 years. This period should align with your financial objectives and responsibilities.

Health Information (in some cases):

- Some calculators may ask for your health-related details to provide a more accurate premium estimate. Your health status can affect the cost of insurance.

Results and Recommendations:

- After entering all the required information, the calculator will generate an estimate of the coverage amount you should consider. This figure represents the financial support your family may need in the event of your death.

How to Use a Term Insurance Calculator

Using a term insurance calculator is relatively simple. Here are the steps to follow:

- Gather Information: Before using the calculator, gather essential information, including your age, annual income, current expenses, existing savings and investments, outstanding debts (like loans or mortgages), and the number of dependents.

- Visit a Reliable Calculator: Go to the website of a reputable insurance company or financial institution that offers a term insurance calculator. Many insurance companies provide free calculators on their websites.

- Enter Your Information: Fill in the required fields on the calculator. Typically, you'll need to provide your age, gender, annual income, expenses, outstanding debts, and the number of dependents.

- Consider Inflation: Account for inflation when calculating your coverage needs. Over time, the cost of living will increase, so you should plan for this by adjusting your coverage amount accordingly.

- Factor in Your Financial Goals: Think about your long-term financial goals, such as funding your children's education, paying off a mortgage, or covering retirement expenses. These objectives should also be considered when determining the coverage amount.

- Review the Results: Once you've entered all the necessary information, the calculator will provide you with an estimated coverage amount. This figure represents the amount of coverage you should consider purchasing.

- Consult with an Advisor: While online calculators are a great starting point, it's a good idea to consult with a financial advisor or insurance expert to fine-tune your coverage needs and choose the right term insurance policy.

Conclusion

A term insurance calculator is a valuable tool that can help you determine the right amount of coverage to safeguard your family's financial future. By considering your current financial situation, expenses, outstanding debts, and long-term goals, you can use this tool to make an informed decision about the coverage you need. Remember that it's essential to review your insurance needs periodically, especially when major life events occur, to ensure your coverage remains adequate. Ultimately, term insurance can offer peace of mind and security to you and your loved ones in times of uncertainty.

About the Author

Introduction

What is Term Insurance?

What is a Term Insurance Calculator?

Components of a Term Insurance Calculator

How to Use a Term Insurance Calculator

Conclusion