Credit Score

Check Your Credit Score

Get instant access to your credit score at no cost. Stay informed and loan-ready.

1.5M+ people

checked their credit Score

Most lenders require a CIBIL score between 700 and 750 to approve a two-wheeler loan at competitive interest rates. But that number only tells part of the story. The minimum CIBIL score for two-wheeler loan approval varies across banks, NBFCs, and captive finance arms of vehicle manufacturers. Some approve applications at 650, while others reject anything below 720. This guide breaks down what different score ranges mean for your bike loan application, how lenders evaluate borderline cases, and practical steps to improve your chances.

Understanding CIBIL Score and Its Role in Bike Loans

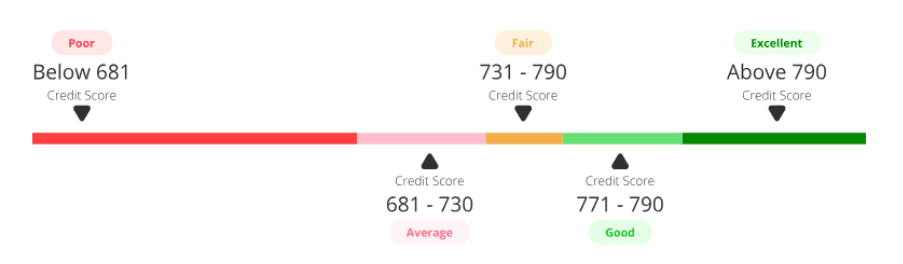

Your CIBIL score is a three-digit number between 300 and 900 that reflects your credit behaviour. Lenders use it as a quick filter before examining your full application. A higher score signals lower risk, which translates to faster approvals and better terms.

For two-wheeler loans specifically, the score carries significant weight because these are typically unsecured or lightly secured loans. Unlike home loans where the property serves as collateral, bike loans rely heavily on your repayment history and income stability, and the minimum Cibil score for bike loan becomes a deciding factor.

How CIBIL Score Affects Your Bike Loan

|

CIBIL Score Range |

Lender Response |

Interest Rate Impact |

|

750 and above |

Quick approval, best terms |

Lowest rates (9% to 12% p.a.) |

|

700 to 749 |

Standard approval process |

Moderate rates (12% to 16% p.a.) |

|

650 to 699 |

Scrutiny, higher down payment |

Higher rates (16% to 20% p.a.) |

|

600 to 649 |

Limited options, guarantor needed |

Highest rates (20% to 24% p.a.) |

|

Below 600 |

Rejection likely |

Most lenders decline |

These ranges are approximate. Individual lenders set their own thresholds based on risk appetite and market positioning.

What is the Minimum CIBIL Score for Bike Loan Approval?

The minimum CIBIL score for two-wheeler loan approval is 650 for many NBFCs. However, the minimum cibil score for bike loan at traditional banks is typically 700 or higher. Their underwriting standards are stricter because they operate under tighter regulatory frameworks and have lower tolerance for defaults.

NBFCs and captive finance companies (like Bajaj Finance, TVS Credit, or Hero FinCorp) often work with scores starting at 650. Some even consider applications at 620 if other factors compensate for the lower score.

Factors that can offset a borderline CIBIL score:

- Stable employment with the same employer for 2+ years

- Higher income relative to the loan amount requested

- Willingness to pay a larger down payment (30% to 40% instead of 10% to 15%)

- Existing relationship with the lender (savings account, FD, or previous loan)

- Adding a co-applicant or guarantor with a strong credit profile

A score of 680 with a 40% down payment might get approved faster than a score of 720 with only 10% down.

CIBIL Score Requirements by Lender Type

Different lender categories apply different standards when evaluating two-wheeler loan applications.

|

Lender Type |

CIBIL Requirement |

Best For |

|

PSU Banks |

700 to 750 |

Lowest interest rates |

|

Private Banks |

680 to 720 |

Existing customers |

|

NBFCs |

650 to 700 |

Flexible eligibility |

|

Manufacturer Finance (Hero FinCorp, TVS Credit) |

625 to 675 |

Brand-specific purchases |

|

Smaller NBFCs |

600 to 650 |

Low-score applicants |

The minimum CIBIL score for two-wheeler loan threshold can vary by more than 100 points across different lender types. Understanding the minimum Cibil score for bike loan across lenders helps you apply strategically and avoid unnecessary rejections. Knowing where to apply saves time and protects your score from unnecessary hard inquiries.

Impact of Low CIBIL Score on Your Bike Loan

Applying for a two-wheeler loan with a score below 700 creates several challenges, especially if you fall short of the minimum Cibil score for bike loan required by banks.

Higher Interest Rates

The most immediate impact hits your wallet. A borrower with a 750 score might pay 10% p.a. on a ₹1 lakh bike loan. The same loan for someone at 650 could carry 18% to 20% rate.

Cost comparison for ₹90,000 loan over 3 years:

|

CIBIL Score |

Interest Rate |

Monthly EMI |

Total Interest Paid |

|

750+ |

10% p.a. |

₹2,903 |

₹14,508 |

|

700 |

13% p.a. |

₹3,033 |

₹19,188 |

|

650 |

16% p.a. |

₹3,163 |

₹23,868 |

|

600 |

20% p.a. |

₹3,343 |

₹30,348 |

Larger Down Payment Requirements

Lenders reduce their exposure to risky borrowers by demanding higher upfront payments when applicants do not meet the minimum Cibil score for bike loan benchmark.

Down payment expectations:

- Standard (score 700+): 10% to 15% of bike value

- Borderline (score 650-699): 20% to 30% of bike value

- Low score (below 650): 35% to 45% of bike value

For a bike costing ₹1.2 lakhs on-road, the difference between 15% and 40% down payment is ₹30,000 extra cash needed upfront.

Limited Lender Options

Major banks simply decline applications below their threshold. Your choices narrow to NBFCs, smaller finance companies, and dealership financing schemes. While these options exist, they come with higher costs.

Can I get bike loan with low CIBIL score?

A score below 700 does not mean automatic rejection. If you're wondering, can I get bike loan with low Cibil score, the answer is yes, but strategy matters. Several approaches improve your approval odds even if you fall short of the minimum Cibil score for bike loan requirement.

Increase Your Down Payment

This is the most effective lever. Paying 30% to 40% upfront reduces the lender's risk substantially.

Calculate what you can afford. If increasing the down payment by ₹20,000 saves you ₹15,000 in interest over the loan tenure, the maths favours paying more upfront.

Apply with a Co-Applicant

Adding a family member with a stronger credit profile changes the risk equation. The lender now has two people responsible for repayment. This directly improves your chances if you do not meet the minimum Cibil score for two-wheeler loan requirement on your own.

Good co-applicant options:

- Spouse with stable income and good credit

- Parent or sibling with established credit history

- Business partner (for self-employed applicants)

Many NBFCs approve loans primarily on the co-applicant's strength when the primary borrower has weak credit.

Choose NBFC Financing Over Banks

NBFCs operate with more flexible criteria. Companies like Bajaj Finance, TVS Credit, Mahindra Finance, and Hero FinCorp specialise in two-wheeler financing and accept a broader range of credit profiles.

Their interest rates run higher than bank rates, but approval chances improve significantly for those asking, can I get bike loan with low Cibil score.

Negotiate with the Dealer

Dealerships often have tie-ups with multiple finance partners. The sales executive can check your eligibility across several lenders simultaneously.

Be upfront about your credit situation. A good salesperson will guide you toward lenders most likely to approve your application if you are slightly below the minimum cibil score for bike loan cutoff.

How to Improve Your CIBIL Score for a Bike Loan

Score below the threshold? Delaying your purchase by 3 to 6 months while fixing credit issues often pays off. The interest savings alone can justify waiting until you comfortably meet the minimum Cibil score for bike loan requirement.

What Works Fast (Within 3 Months)

Start with EMI discipline. Not a single late payment. Even one missed due date drags your score down by 50 to 100 points.

Credit card balances matter more than most people realise. Using 80% of your limit screams financial stress to the algorithm. Drop that to 25% or less. Pay mid-cycle if needed.

Got overdue amounts sitting anywhere? Clear them first. Aged defaults hurt worse than recent ones, but any outstanding debt signals risk.

Check your CIBIL report for errors too. Wrong entries happen surprisingly often. Dispute through the portal and corrections show up in 30 to 45 days.

Building Credit Over 3 to 6 Months

Stop applying for new credit entirely. Each application creates a hard inquiry that chips away at your score.

Boring consistency wins here. Same low utilisation month after month. Every EMI paid before the deadline. No drama, no excuses.

If you lack credit history, a secured card against your FD builds a track record without risk of rejection.

Realistic Timeline for Score Recovery

Three months of clean behaviour typically adds 30 to 50 points. Six months can mean 50 to 100 points improvement. Major turnarounds from very low scores take a year or longer.

Worth waiting? Absolutely. Moving from NBFC rates at 18% to bank rates at 10% saves thousands over your loan tenure.

Check Your Credit Report for Errors

Request your free annual CIBIL report and review every entry. Common errors include:

- Loans marked as active that you already closed

- Incorrect payment status showing delays that never happened

- Duplicate entries for the same account

- Identity mix-ups with someone having a similar name

Dispute errors through the CIBIL portal. Corrections typically reflect within 30 to 45 days and can boost your score immediately.

Other Ways to Finance Your Bike

Bike loan rejections happen. That does not end your options.

Cash Through a Personal Loan

Here is an angle most dealers will not mention. Walk in with cash and your negotiating power multiplies. Personal loans from NBFCs convert credit into buying power without the bike being hypothecated.

Finnable's personal loans start at ₹50,000 and go up to ₹10 lakhs. Is CIBIL’s threshold limit just 675, the answer is noit is a bit highr. Processing happens fast too. Some borrowers see funds in their account within 60 minutes of approval. Rates fall between 15% and 30.99% p.a. based on individual profiles.

The maths often works out better than high-interest bike financing. Plus you own the vehicle outright from day one.

Pledge Gold Instead

Gold sitting in your locker? Banks and NBFCs will lend against it without checking CIBIL at all. Zero score requirements. Rates hover around 7% to 15% p.a., which beats most two-wheeler financing for low-score borrowers by a wide margin.

Catch: you cannot wear or use the pledged jewellery until repayment. Fair trade for affordable credit though.

Just Save and Wait

Not glamorous advice, but practical. Putting away ₹5,000 monthly builds ₹60,000 in a year. That amount covers 50% down payment on many popular bikes.

Meanwhile, your credit recovers. Twelve months of clean payment behaviour can add 100 points to your score. The bike you buy next year costs significantly less in interest than the one you finance today at 20% rates.

Documents Required for Bike Loan Application

Identity and Address Proof:

- Aadhaar card

- PAN card (mandatory)

- Passport or Voter ID

- Utility bills for address verification

Income Proof (Salaried):

- Salary slips for last 3 months

- Bank statements for 3 to 6 months

- Form 16 or ITR

Income Proof (Self-Employed):

- ITR for last 2 years

- Bank statements for 6 to 12 months

- Business registration documents

Additional for Low CIBIL Applicants:

- Guarantor documents

- Asset ownership proof

- lAdditional income documentation

Making Your Two-Wheeler Purchase Happen with Finnable

The minimum CIBIL score for bike loan depends heavily on lender choice and overall profile strength. Applicants with scores below standard thresholds can still succeed through strategic lender selection, increased down payments, and co-applicant addition.

For those needing funds beyond bike financing, Finnable offers personal loans starting from ₹50,000 with flexible eligibility criteria. The minimum Cibil score for two-wheeler loan is 675 or may differ and disbursal in as little as 60 minutes makes it a practical option for various financial needs including vehicle purchases. Finnable evaluates applicants based on income stability and employment profile, making it accessible even for those just starting their credit journey."

Difficult but possible. You will need a substantial down payment (35% to 40%), possibly a co-applicant, and will likely pay higher interest rates (18% to 24% p.a.). Focus on NBFCs like Hero FinCorp or TVS Credit rather than banks.

Correcting errors reflects in 30 to 45 days. Paying down debt and maintaining on-time payments can boost scores by 50 to 100 points within 3 to 6 months. Major improvements from very low scores may take 12 to 18 months.

The application creates a hard inquiry, dropping your score by 5 to 10 points temporarily. The rejection itself is not recorded on your report. However, multiple applications in a short period signal desperation and cause cumulative damage.

NBFCs rather than banks offer the lowest thresholds. Hero FinCorp and TVS Credit (for their respective brands) often approve from 625 and above. Bajaj Finance considers 650 and above. For existing bank customers with good account history, some private banks approve from 680.

Not always mandatory, but it significantly improves approval chances. Lenders view a guarantor as additional security against default. The guarantor should have a CIBIL score above 700 and stable income.

Depending on your CIBIL score and monthly income, the interest charged on the loan will be between 16% to 26%

As an RBI regulated NBFC, we are required to follow the procedures which include getting KYC documents from our customer’s. So, it is mandatory to submit documents to get a loan online.

Yes, extremely safe. Finnable is an RBI regulated NBFC

Credit Score

Check Your Credit Score

Get instant access to your credit score at no cost. Stay informed and loan-ready.

1.5M+ people

checked their credit Score

Understanding CIBIL Score and Its Role in Bike Loans

How CIBIL Score Affects Your Bike Loan

What is the Minimum CIBIL Score for Bike Loan Approval?

CIBIL Score Requirements by Lender Type

Impact of Low CIBIL Score on Your Bike Loan

Can I get bike loan with low CIBIL score?

How to Improve Your CIBIL Score for a Bike Loan

Check Your Credit Report for Errors

Other Ways to Finance Your Bike

Documents Required for Bike Loan Application

Making Your Two-Wheeler Purchase Happen with Finnable