-

Can I convert a term insurance policy into a life insurance policy?

Some insurers in India offer conversion options from term to whole life or endowment plans, although this might come with added conditions and charges.

-

Which is more affordable in the long run?

If you’re looking for pure risk coverage at an economical price, term insurance is more affordable. However, life insurance provides additional benefits that justify its higher premium.

-

Is term insurance better for young individuals?

Term insurance is particularly suitable for young earners with financial dependents, as it offers high coverage at lower premiums.

-

Does life insurance have tax benefits?

Yes, under Section 80C, premiums paid towards life insurance are eligible for deductions, while the maturity amount and death benefit are generally exempt under Section 10(10D).

Understanding the Difference Between Life Insurance and Term Insurance

Loan in

60 Minutes

Introduction

When it comes to safeguarding your family's financial future, choosing the right insurance plan is crucial. However, deciding between life insurance and term insurance can be a challenge for many in India. While these terms are often used interchangeably, they are distinct in their benefits, duration, and structure. In this blog we will explore the difference between life insurance and term insurance, helping you understand which one might be the better fit for your needs.

What is Life Insurance?

Life insurance is a comprehensive financial instrument designed to provide a death benefit to the beneficiary, along with additional components such as bonuses, maturity benefits, and savings accumulation. Typical types of life insurance in India include Whole Life Insurance and Endowment Plans. Life insurance is often selected by individuals who seek long-term financial security and wish to create a wealth-building tool along with coverage.

What is Term Insurance?

Term insurance, on the other hand, is straightforward insurance coverage with a limited duration. Unlike life insurance, term insurance offers only the death benefit to beneficiaries if the insured passes away within the policy's tenure. Term insurance provides pure risk coverage without any savings or maturity benefits, making it a simpler, more affordable option.

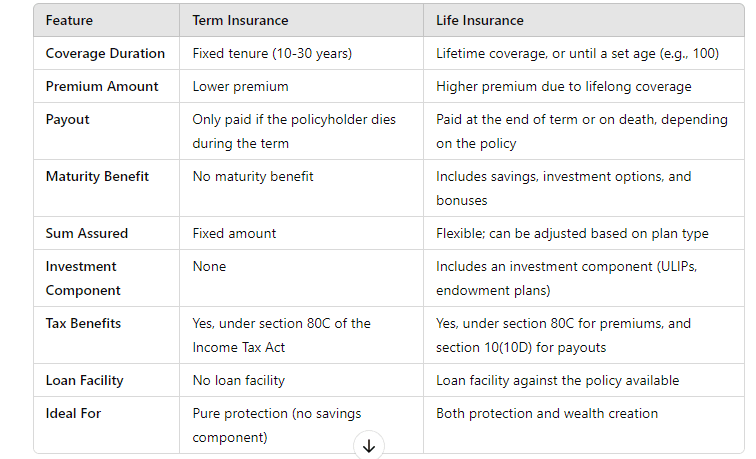

Key Differences Between Life Insurance and Term Insurance

Coverage Duration and Benefits

Life Insurance : Generally, life insurance covers the insured for their entire life or until a specific age (such as 99 or 100). At the end of the policy term or upon the policyholder’s death, a maturity benefit or death benefit, respectively, is provided to the beneficiaries. Whole life plans often provide cash value accumulation, which can be a significant draw for those looking for an investment component.

Term Insurance : Term insurance typically offers coverage for a predetermined term, ranging from 5 to 30 years. If the policyholder dies within the term, the beneficiaries receive the death benefit. However, no maturity or survival benefits are included. This type of insurance is ideal for individuals looking to cover specific financial obligations, like loans or children’s education costs, within a limited timeframe.

Premium Costs

Life Insurance : The premiums for life insurance policies are usually higher than those of term insurance. This is due to the dual nature of life insurance, which combines coverage and savings components, resulting in higher charges. Policies like endowment plans are particularly popular for their long-term savings advantage, but they come at a greater cost.

Term Insurance : Term plans have a significantly lower premium since they cover only the risk of death without additional benefits. These low-cost premiums make term plans an affordable option, especially for young policyholders who want comprehensive protection at a reasonable rate.

Return on Investment and Cash Value

Life Insurance : Life insurance often includes an investment component. Many policies accrue a cash value that the policyholder can access during the term. Over time, life insurance can thus act as a savings instrument and may include bonuses and guaranteed returns. Life insurance policies in India also allow policyholders to borrow against the cash value, adding liquidity.

Term Insurance : Since term insurance offers no cash value or savings aspect, there is no investment return. The sole purpose of term insurance is to provide a safety net to dependents in the event of the policyholder’s death.

Policy Features and Flexibility

Life Insurance : Life insurance policies offer a variety of features, such as partial withdrawals, surrender value, and even the option to convert a term policy to a whole-life plan in some cases. Endowment and whole-life plans also offer maturity benefits and are considered flexible in terms of policyholder options for fund access.

Term Insurance : Term policies are generally more rigid; they do not include options like withdrawals or maturity benefits. While some companies now offer return-of-premium (ROP) options for term insurance, this is often at a higher premium and still lacks the investment benefits of a standard life insurance policy.

Why Opt for Term Insurance?

- Affordability : Since term insurance provides pure risk coverage, the premiums are far lower than those of life insurance policies, making it an affordable option for individuals who need large coverages, such as young professionals with dependents.

- Focused Protection : Term plans are designed to cover specific needs, such as loans, education expenses, or short-term financial goals.

- Tax Benefits : Premiums paid towards term insurance qualify for tax deductions under Section 80C of the Income Tax Act, and the death benefit received is also tax-exempt under Section 10(10D).

Why Choose Life Insurance?

- Lifetime Coverage : Whole life insurance covers policyholders until death, offering long-term security and financial support to family members, especially valuable for estate planning.

- Wealth Creation : Life insurance combines investment with coverage. Through bonuses, maturity benefits, and other returns, policyholders can accumulate significant savings over time.

- Flexibility and Loan Option : Life insurance policies can be utilized as collateral for loans, and some plans allow partial withdrawals or surrendering the policy if needed, giving the policyholder financial flexibility.

Conclusion

Choosing between life insurance and term insurance in India depends on your financial goals, coverage needs, and budget. While term insurance offers affordable, straightforward coverage for a specific term, life insurance provides lifetime coverage, savings, and investment benefits. A well-informed choice will ensure you’re protecting your loved ones while also aligning with your financial strategy.

For detailed insights and current policy options, visit consult financial platforms online, where you can compare the best plans available in the Indian insurance market.

FAQs

Introduction

What is Life Insurance?

What is Term Insurance?

Key Differences Between Life Insurance and Term Insurance

Coverage Duration and Benefits

Premium Costs

Return on Investment and Cash Value

Policy Features and Flexibility

Why Opt for Term Insurance?

Why Choose Life Insurance?

Conclusion

FAQs