Loan in

60 Minutes

Introduction

Owning a home is a dream for many in India, and to turn this dream into reality, individuals often explore various financial options, including their Employees' Provident Fund (EPF). The EPF is a long-term savings scheme established by the Indian government to provide financial security to employees after retirement. While the primary purpose of EPF is retirement savings, there are certain provisions that allow partial withdrawal for specific purposes, such as buying or constructing a house. Yes, you can conduct PF withdrawal for a home loan in India under certain conditions.

The EPFO (Employees' Provident Fund Organization) allows members to make partial withdrawals from their EPF accounts to finance the purchase or construction of a house. This facility is provided under the EPF Scheme 1952.

Conditions for Withdrawing PF for a Home Loan

If you wish to withdraw from your EPF to meet your home loan requirements, you must qualify for the following conditions:

-

Eligibility: To be eligible for EPF withdrawal for a home loan, you must have completed at least three years of continuous service. The accumulated EPF balance, including both your and your employer's contributions along with interest, can be used.

-

Property Ownership: You can use EPF funds to purchase or construct a house only if you or your spouse or jointly own the property. This means that EPF withdrawals are not allowed for buying a property solely in the name of a family member other than your spouse.

-

Withdrawal Limit: You can withdraw up to 90% of your EPF balance for the purpose of purchasing or constructing a house. This includes the cost of land, if applicable. The remaining 10% must be left in your EPF account.

-

Minimum Service Period: EPF withdrawals for a home loan are typically allowed after five years of service. However, in cases of special circumstances such as a change of job, this period can be reduced to three years.

-

Property Ownership Period: Once you withdraw EPF for a home loan, the purchased property should remain in your ownership for at least five years. If you sell the property within this period, the withdrawn amount will be treated as taxable income, and you will need to pay tax on it.

Procedure for Withdrawing PF for a Home Loan

If you have decided to withdraw from your PF to pay for your home loan, you can make the request for the same either through the EPFO website or the UMANG App. However, before you begin the process, make sure you have all the details with you:

- Unified Account Number (UAN)

- Aadhaar

- PAN

- Bank Account Number

- Scanned Copy of the Cheque

- Employer’s Details

- Home Loan Sanction Letter

Using the EPF Website:

Step 1- Visit the EPFO Member Portal: Go to the official EPFO member portal at https://unifiedportal-mem.epfindia.gov.in/memberinterface/.

Step 2- Log In: Log in using your Universal Account Number (UAN) and password. If you haven't activated your UAN or set a password, you can do so on the portal.

Step 3- Verify KYC Details: Ensure that your Know Your Customer (KYC) details such as Aadhar, PAN, and bank account details are linked and verified with your UAN.

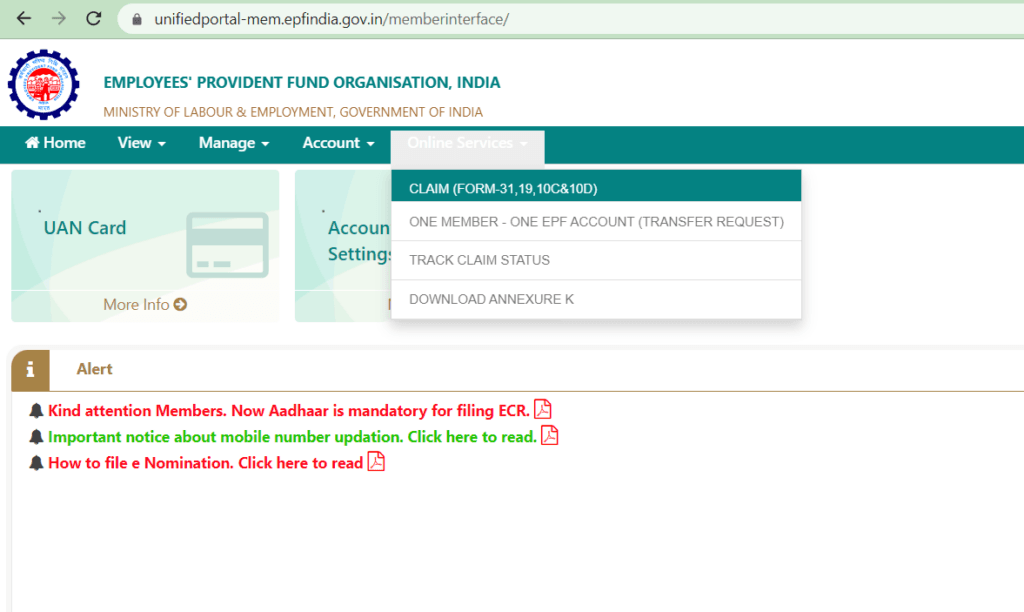

Step 4- Select 'Online Services': From the main menu, click on 'Online Services.'

Step 5- Choose 'Claim (Form-31, 19, 10C & 10D)': Under the 'Online Services' menu, select 'Claim (Form-31, 19, 10C & 10D)' to start the withdrawal process.

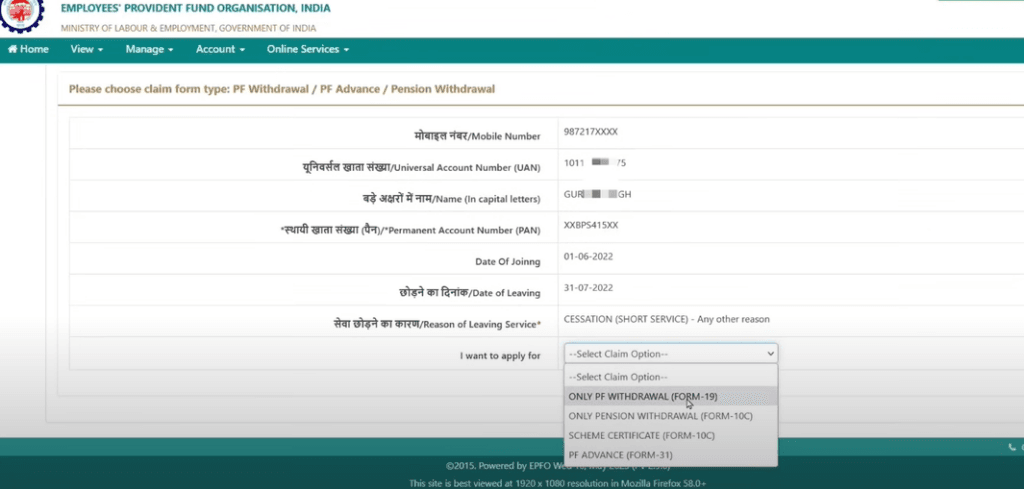

Step 6- Verify Personal Details: Verify your personal details, including your bank account number, and click on 'Proceed for Online Claim.'

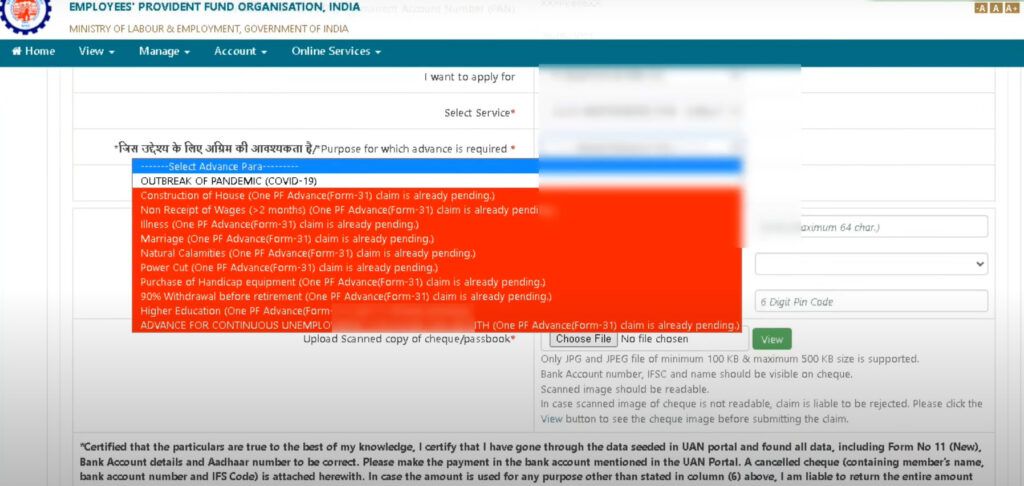

Step 7- Select 'PF Advance (Form 31)': From the dropdown menu, choose 'PF Advance (Form 31)' as the type of claim you wish to make.

Step 8- Purpose of Withdrawal: Select 'Purpose for which advance is required' as 'Purchase of House Site/Flat' to withdraw for a home loan.

Step 9- Complete the Application: Fill in the required details such as your address, the amount required, and the employer's details. Also, upload the necessary documents, including the home loan sanction letter.

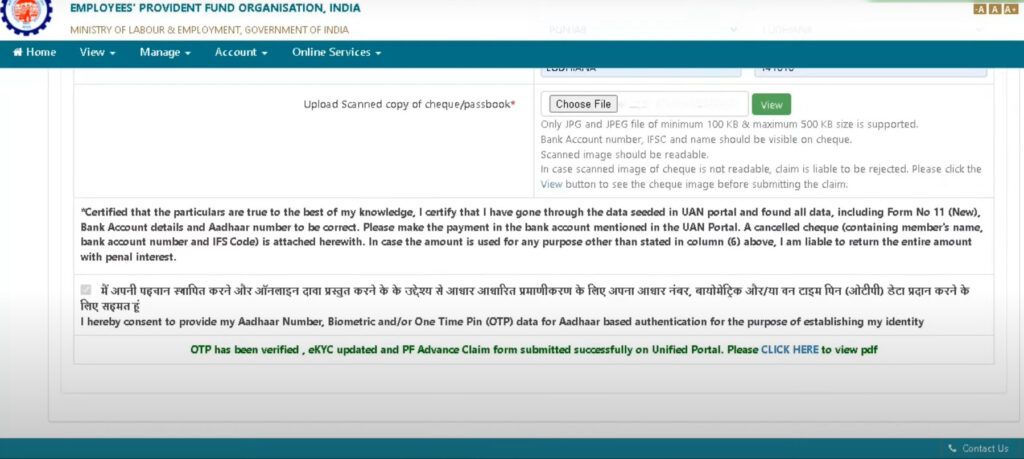

Step 10- Submit Your Claim: After completing the application, click on 'Get Aadhar OTP' and validate it. Then, submit your claim. You'll receive an OTP on your registered mobile number for verification.

Using the UMANG App:

Step 1- Download the UMANG App: Download and install the UMANG (Unified Mobile Application for New-age Governance) app from your device's app store.

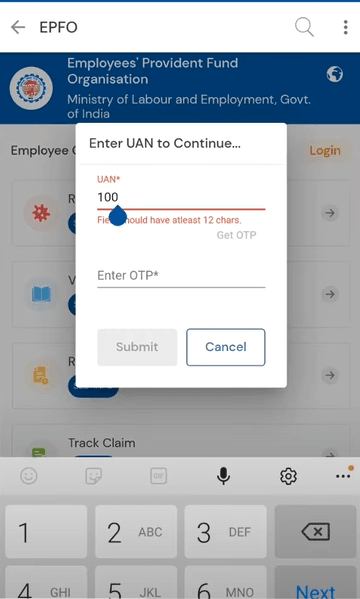

Step 2- Open UMANG: Launch the UMANG app and select the 'EPFO' service among the various government services available.

Step 3- Login or Register: Log in using your UAN and password. If you haven't registered, you can do so within the app.

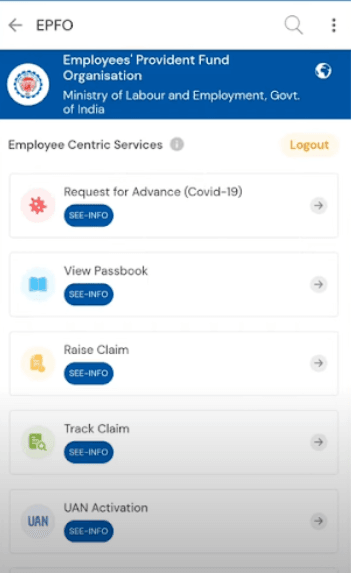

Step 4- Access 'Online Services': Once logged in, access the 'EPFO Services' section within the app.

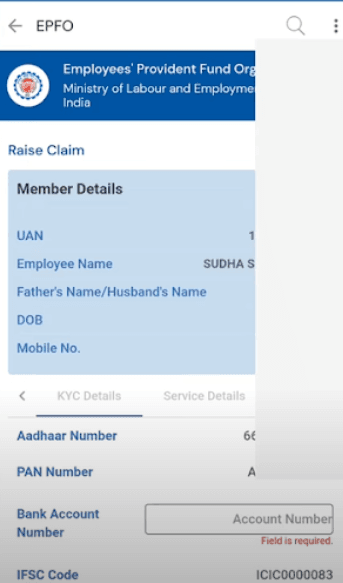

Step 5- Select 'Raise Claim’: Choose the 'Raise Claim ' to initiate the withdrawal process.

Step 6- Verify Personal Details: Verify your personal details, bank account number, and Aadhar, and click 'Proceed for Online Claim.'

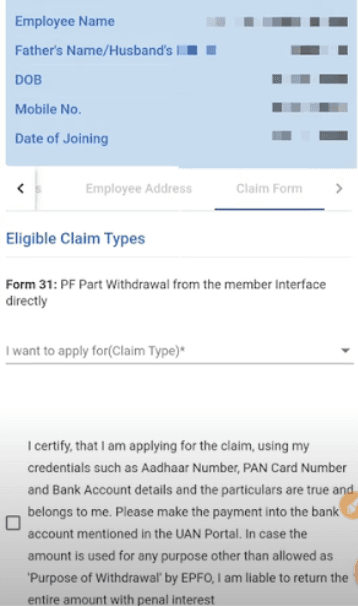

Step 7- Choose 'PF Advance (Form 31)': From the list of services, select 'PF Advance (Form 31)' as the type of claim you want to make.

Step 8- Specify Purpose: Indicate that you're withdrawing for the 'Purchase of House Site/Flat.'

Step 9- Complete Application: Fill in the required information and upload the necessary documents, including the home loan sanction letter.

Step 10- Submit Claim: After filling out the application, submit it. An OTP will be sent to your registered mobile number for verification.

Use TrackMyPF to Withdraw Your PF

Finnable’s TrackMyPF app allows you to check and withdraw your PF balance. Follow these steps to withdraw PF using TrackMyPF:

-

Download the App: Download and install the TrackMyPF Balance App from the Play Store or Apple Store.

-

Sign up/Login to the App: Sign up to the app using your mobile number. If you already have an account, log in to the app using your UAN and password.

-

Navigate to Withdrawal Section: Under My Account, locate the Withdraw Balance section and click on it.

-

Fill in the Required Details: Complete the withdrawal form with the necessary details. Ensure accuracy in providing information.

-

Attach Required Documents: Attach supporting documents required for withdrawal, such as a canceled cheque, KYC documents, and any other relevant paperwork.

-

Submit the Claim: Once the form is filled and documents are attached, submit the withdrawal claim through the app.

-

Track the Withdrawal Status: You can also track the status of your withdrawal request on the app. The processing time may vary.

Conclusion

Withdrawing EPF for a home loan in India is a viable option if you meet the specified conditions. It can provide you with the necessary financial assistance to fulfill your dream of owning a home. However, it’s essential to understand the rules and regulations governing EPF withdrawals and ensure that you comply with the eligibility criteria and ownership requirements. Additionally, remember that while EPF withdrawals offer financial flexibility, they reduce your retirement savings, so it’s essential to strike a balance between your immediate and long-term financial goals.

Loan in

60 Minutes

Introduction

Conditions for Withdrawing PF for a Home Loan

Procedure for Withdrawing PF for a Home Loan

Use TrackMyPF to Withdraw Your PF

Conclusion