A Complete Guide to Cibil Score Correction in India

Introduction

Your CIBIL score is more than just a number; it’s the key to unlocking financial opportunities like loans and credit cards. If you’ve recently found yourself in a situation where your score has dipped, don’t worry—you’re not alone, and the situation is fixable.

With the right approach and consistent effort, you can rebuild your creditworthiness and regain access to the financial avenues you need to achieve your goals. This blog will walk you through the steps for Cibil Score Correction, ensuring you’re equipped to take charge of your financial health.

Why Does Your CIBIL Score Matter?

Your CIBIL score reflects your creditworthiness and is used by lenders to assess your eligibility for financial products. In India, a good CIBIL score, typically above 750, can open doors to lower interest rates, faster approvals, and better credit terms. However, errors or financial missteps can negatively impact your score, making Cibil Score Correction a crucial step in regaining financial stability.

What Causes a Low CIBIL Score?

Before diving into solutions, it’s important to understand the common factors that might have caused your score to drop:

-

Missed Payments: Delayed or skipped loan or credit card payments significantly affect your score.

-

High Credit Utilization Ratio: Using a large percentage of your credit limit indicates over-reliance on borrowed money.

-

Multiple Loan Applications: Frequent hard inquiries from lenders can lower your score.

-

Errors in Credit Report: Mistakes like incorrect loan details or repayments not being recorded can bring your score down.

-

Defaulting on Loans: Not paying EMIs on time can have a long-term impact on your score.

Steps for Effective Cibil Score Correction

Here’s a structured plan to help you improve your credit score:

1. Check Your Credit Report Regularly

Start by obtaining a copy of your credit report from CIBIL or other credit bureaus like Experian or Equifax. Look for discrepancies such as:

- Incorrect personal information

- Unrecorded payments

- Accounts or loans that you don’t recognize

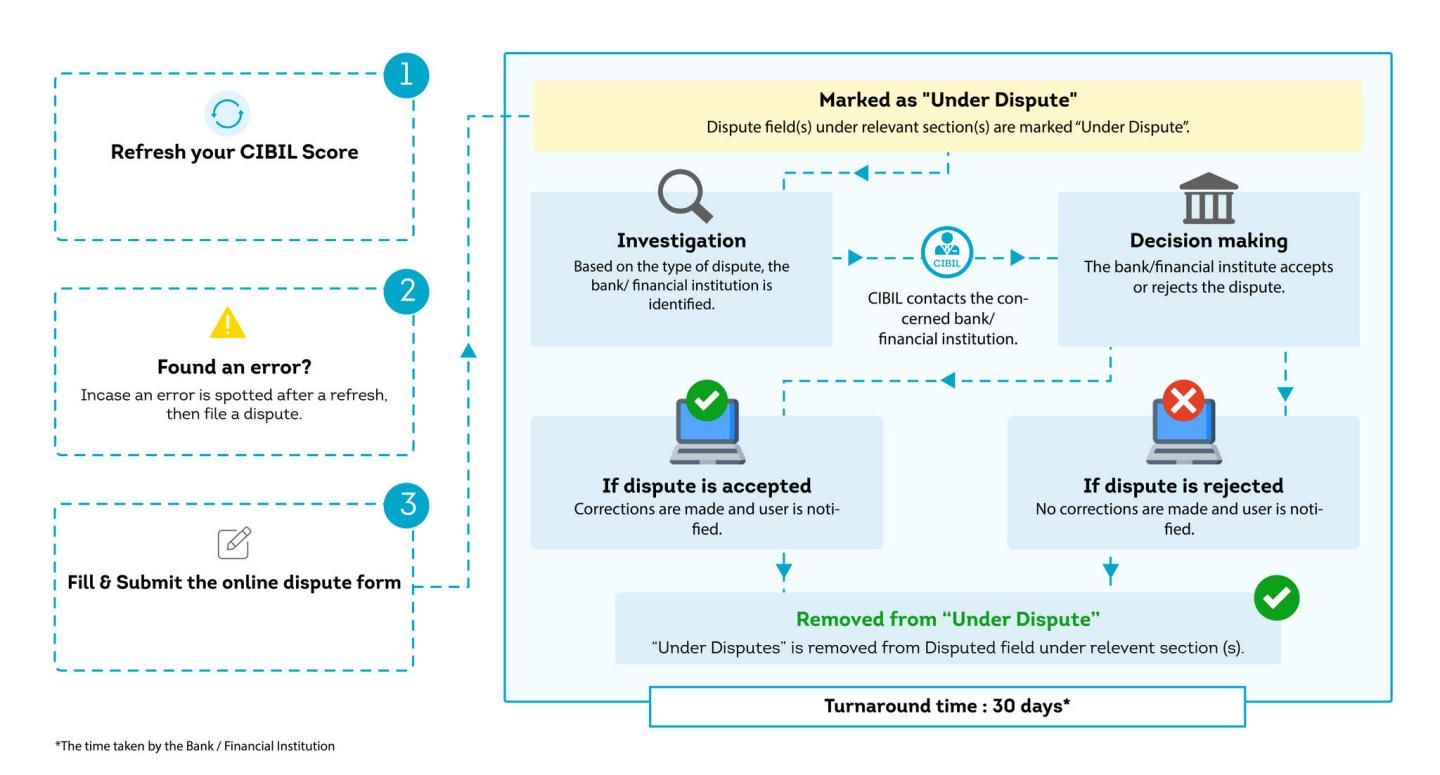

2. Dispute Errors

If you spot any errors, initiate a dispute with the credit bureau immediately. Follow these steps for a smooth dispute resolution:

- Log in to the official CIBIL website.

- Navigate to the “Dispute Resolution” section.

- Provide details of the error and upload supporting documents.

- Track your dispute status online.

3. Clear Outstanding Debts

Pay off any pending dues, starting with high-interest debts. If you’re unable to pay in full, negotiate with your lender for a settlement or payment plan.

4. Optimize Credit Utilization

Keep your credit utilization below 30% of your total credit limit. For example, if your credit limit is Rs 1,00,000, try not to exceed Rs 30,000 in outstanding dues.

5. Avoid Multiple Loan Applications

Too many applications can result in hard inquiries, which temporarily lower your score. Apply for credit only when necessary.

6. Use a Mix of Credit Products

Maintain a healthy mix of secured (home or car loans) and unsecured (personal loans, credit cards) credit products to show balanced credit behavior.

7. Set Up Payment Reminders

Automate your EMI and credit card payments to ensure timely repayments.

How Long Does Cibil Score Correction Take?

Improving your CIBIL score is a gradual process. Depending on the severity of the issue, it might take:

-

1–3 months: For minor corrections or disputes.

-

6–12 months: For significant improvements through disciplined financial behavior.

The process of CIBIL Score Correction in a nutshell:

Benefits of Cibil Score Correction

Correcting your CIBIL score offers multiple advantages:

-

Faster Loan Approvals: A high score simplifies the approval process.

-

Better Interest Rates: Lenders offer lower interest rates to individuals with good scores.

-

Improved Credit Limits: You can access higher credit limits on credit cards.

Conclusion

CIBIL Score Correction is not a one-time task but an ongoing commitment to financial discipline. Whether you’re addressing errors in your report or adopting healthier financial habits, each step brings you closer to a stronger credit profile. Remember, a good CIBIL score is not just a number; it’s your gateway to financial freedom.

Whether you’re looking for easy-to-access loans, guidance on optimizing your credit usage, or advice on maintaining a healthy financial portfolio, taking proactive steps can make all the difference. Regular monitoring, timely payments, and strategic financial decisions ensure your credit score remains a valuable asset for your future.

FAQs

-

How often should I check my credit report?

It’s advisable to review your credit report every 3–6 months to catch errors early.

-

Can I correct my CIBIL score on my own?

Yes, you can independently review and dispute errors. However, for complex issues, consider seeking professional help.

-

Will closing old credit cards improve my score?

Not necessarily. Older credit accounts with good repayment history boost your score. Closing them might reduce your credit age, impacting your score negatively.

-

Does settling a loan impact my CIBIL score?

Settlements are recorded as “settled” accounts, which can negatively impact your score. Full repayment is always better.

-

How much does it cost to correct a CIBIL score?

Accessing your credit report costs approximately Rs 550 while disputing errors is free. Some third-party services charge fees for additional assistance.

Introduction

Why Does Your CIBIL Score Matter?

What Causes a Low CIBIL Score?

Steps for Effective Cibil Score Correction

How Long Does Cibil Score Correction Take?

Benefits of Cibil Score Correction

Conclusion

FAQs