Cruise the Streets in Confidence with Car Insurance on EMI

Loan in

60 Minutes

Introduction

In the hustle and bustle of modern life, owning a car has transcended mere luxury; it's become an indispensable part of our existence. Beyond the comfort and freedom it provides as we glide through our daily lives, car ownership brings with it a profound responsibility, protecting not just our prized vehicles but also ensuring our own security in the face of unforeseen events. Herein lies the profound significance of car insurance on EMI. Car insurance on EMI not only offers financial protection but also peace of mind. It covers expenses related to accidents, theft, damage, and third-party liabilities, ensuring that you don't have to bear the entire financial burden on your own.

And now, with the option of paying for car insurance on EMI (Equated Monthly Instalments), getting the coverage you need has become more accessible and manageable than ever!

What Is Car Insurance on EMI?

Depending on the model and age of your car, car insurance can cost Up to Rs. 30,000 in India, if not more. However, car insurance on EMI is a payment option that allows you to spread the cost of your insurance premium over monthly installments instead of paying a lump sum amount upfront. This flexible payment arrangement makes it easier for you as a car owner to budget for your insurance expenses without straining your finances.

How to Get Car Insurance on EMI?

The procedure to get car insurance on EMI is simple. Follow these few easy steps to be financially secured as you drive down the road:

Select an Insurance Provider:

Choose a reputable insurance company that offers car insurance on EMI. Research their policies, coverage, and terms to find the best fit for your needs.

Calculate Premium:

The insurer will calculate your annual premium based on factors like your car's make and model, your location, and your driving history. You can use online car insurance premium calculators to estimate the exact cost of your yearly premium.

Choose EMI Plan:

Select the EMI plan that suits your budget. Common options include monthly, quarterly, or semi-annual payments.

Documentation:

Complete the necessary documentation and provide any required financial information to set up the EMI arrangement. These documents may include:

- Proof of identity (e.g., driver's license, passport)

- Proof of address (e.g., utility bill, rental agreement)

- Vehicle registration certificate (RC)

- Previous insurance details (if applicable)

- Income proof or financial statements (for some EMI plans)

- Bank account details for EMI setup

Payment Setup:

The insurance company will set up the payment plan, and the premium amount will be automatically deducted from your bank account on the specified dates.

Car Insurance on EMI in India

The following insurance providers offer car owners the option to pay off their car insurance on EMI:

| Insurance Provider |

| ZestMoney Royal Sundaram |

| Poonawalla Fincorp |

| Kotak General Insurance |

| HDFC Ergo |

| Bajaj Finserv |

Note that all insurance providers offer car insurance on EMI according to traditional loan terms. Therefore, please contact the above listed providers to inquire about their car insurance on EMI options before you proceed with the purchase.

How to Calculate Your Car Insurance EMI?

Once you have calculated the yearly car insurance premium for your car, you can use tools like Bajaj Finserv’s EMI Network or Royal Sundaram’s Anything on EMI services to convert your yearly payments into smaller and more manageable monthly payments. Follow these steps to convert your EMi insurance into a loan:

Step 1 : Wisely Choose Your EMI Network Provider

Begin by selecting a reputable loan provider that offers car insurance on EMI services. Research and compare the available options to get the lowest interest rates to ensure you don’t pay more than you have to.

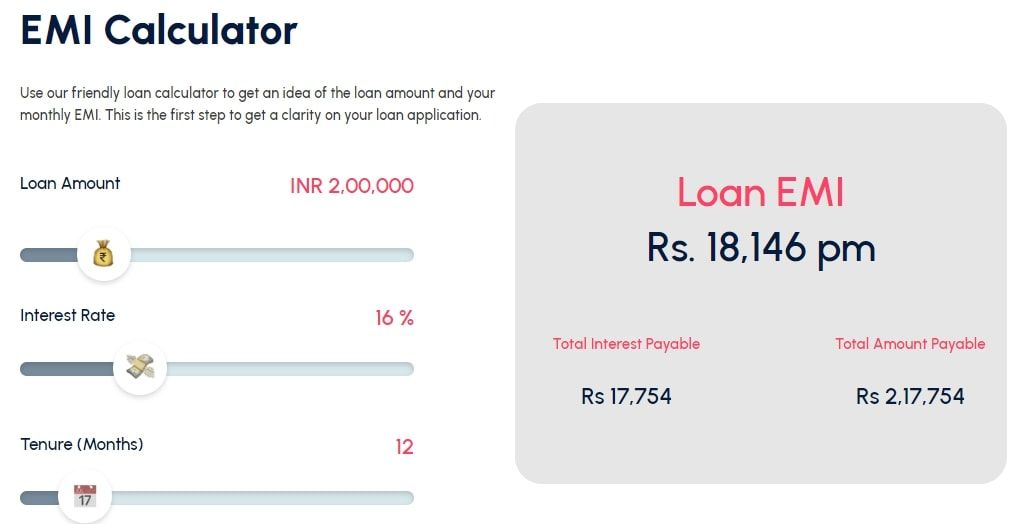

Step 2 : Use an Online EMI Calculator

You can find many EMI calculators that can help you calculate your EMI amount for insurance. This tool allows you to input your premium amount and desired repayment tenure to determine the monthly EMI amount.

Step 3 : Enter Your Premium Amount

Input the annual premium amount quoted by your insurance company into the EMI calculator. Ensure accuracy to obtain precise EMI calculations.

Step 4 : Select Repayment Tenure

Choose a repayment tenure that suits your financial situation. EMI tenures typically range from a few months to a year or more, depending on the provider and the terms of your policy.

Step 5 : Review EMI Details

After entering the necessary details, the EMI calculator will display your monthly installment amount. Take a moment to review the EMI amount, tenure, and any additional charges or fees.

Step 6 : Apply for EMI Conversion

Once you are satisfied with the calculated EMI amount, proceed to apply for the EMI conversion. Follow the provider's instructions for initiating the process, which may involve submitting relevant documents and completing any required paperwork.

Step 7 : Approval and Setup

Upon approval, the EMI setup will be finalized, and the agreed-upon monthly installments will be automatically debited from your bank account on the specified due dates.

Step 8 : Monitor Your Payments

Keep track of your EMI payments and ensure that your bank account has sufficient funds to cover each installment. Timely payments are essential to maintain continuous car insurance coverage.

Conclusion

Car insurance on EMI is an excellent solution for you if you want to protect your vehicles and life without straining your finances. It ensures that you have coverage when you need it most while allowing you to manage your expenses effectively. So, whether you're a seasoned car owner or a first-time driver, consider exploring car insurance on EMI options to experience the convenience and peace of mind it offers.

Introduction

What Is Car Insurance on EMI?

How to Get Car Insurance on EMI?

Car Insurance on EMI in India

How to Calculate Your Car Insurance EMI?

Conclusion