Loan in

60 Minutes

Introduction

The Employee Provident Fund (EPF) is a crucial retirement savings scheme in India that offers financial security to employees during their post-retirement years. While EPF is primarily meant to be a long-term investment, certain situations may arise when individuals need to withdraw funds before retirement. However, it's essential to understand the EPF withdrawal rules to avoid any financial implications. Let us have a detailed look at the EPF withdrawal rules in India.

EPF Withdrawal Eligibility Criteria

The EPF is overseen by the Employees’ Provident Fund Organization (EPFO), which has set certain restrictions on EPF withdrawal. Employees’ Provident Fund (EPF) and Voluntary Provident Fund (VPF) are two types of PF accounts. As such, EPF is a mandatory contribution by both employees and employers, while the VPF is a voluntary contribution made by employees above the statutory limit. To withdraw from EPF or VPF, certain criteria must be met:

-

Retirement: The primary purpose of EPF is to provide financial security during retirement. Therefore, an employee can withdraw the full EPF balance upon reaching the age of 58 or retiring from regular employment.

-

Continuous Unemployment: If an employee remains unemployed for two months or more, they can withdraw the EPF balance.

-

Marriage: Employees can withdraw up to 50% of their EPF balance for their marriage or the marriage of their children, subject to certain conditions.

-

Education: Partial withdrawal rules allow for the employee’s or their children’s higher education.

-

Medical Emergency: In case of a medical emergency, employees can withdraw a portion of their EPF balance.

-

Home Loan Repayment: EPF can be used for the partial or full repayment of a home loan after five years of service.

EPF Withdrawal Rules and Process (Website)

The EPF withdrawal process in India has become more convenient and streamlined over the years, thanks to various digital initiatives introduced by the EPFO. Employees can now apply for partial or complete EPF withdrawal online through the EPFO member portal. Below is a step-by-step guide to the EPF withdrawal process:

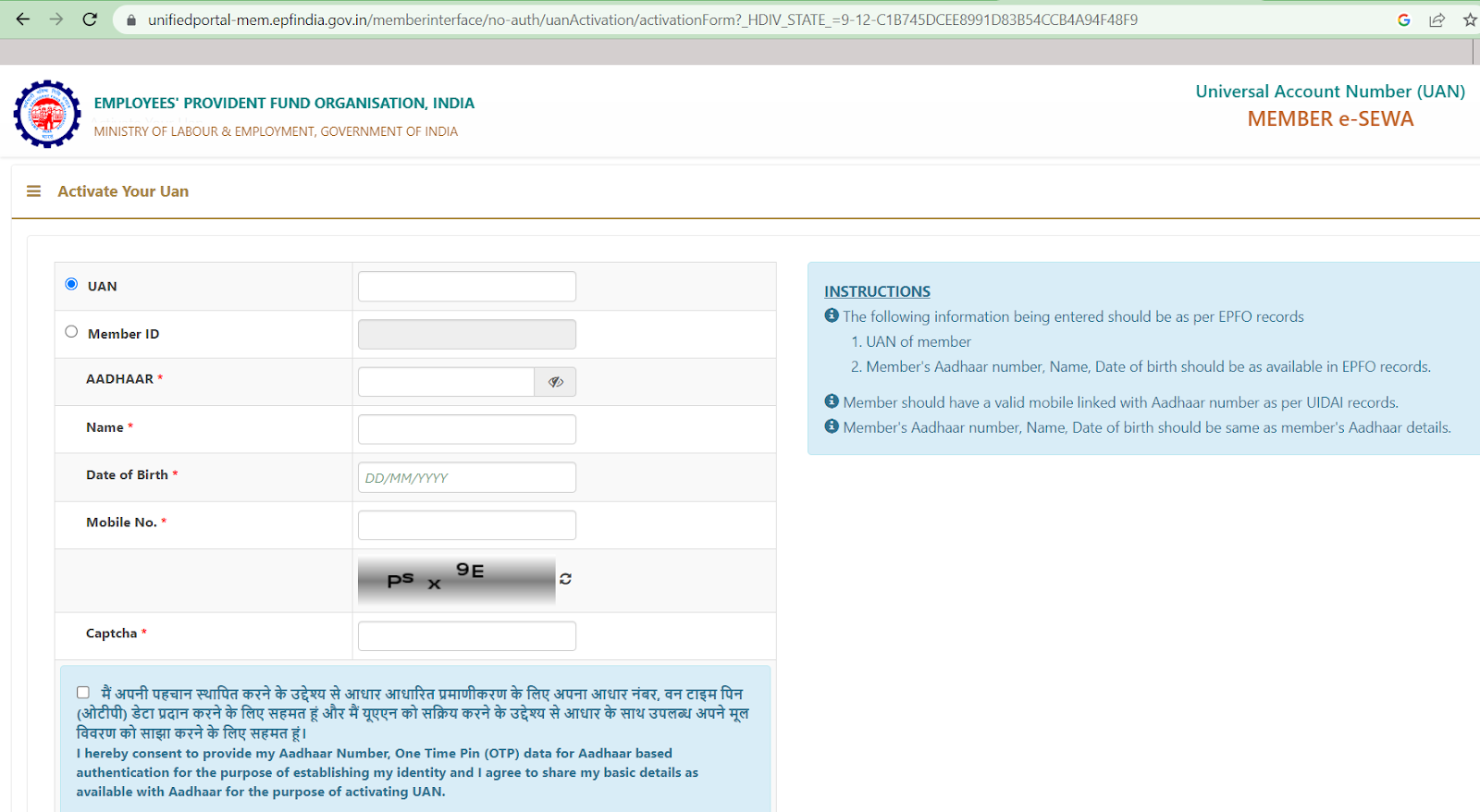

Step 1: UAN Activation

Before initiating the EPF withdrawal process, ensure that your Universal Account Number (UAN) is activated. The UAN is a unique 12-digit number assigned to every EPF account holder. If you haven’t activated your UAN, contact your employer to obtain the UAN or complete the activation process on the EPFO’s UAN activation portal.

Step 2: Login to EPFO Member Portal

Visit the EPFO member portal and login using your UAN and password. If it’s your first time logging in, the portal will prompt you to change your password for security reasons.

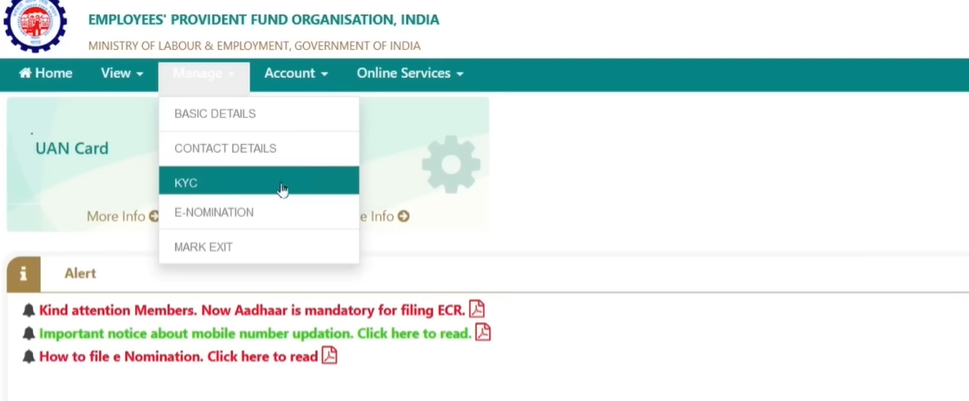

Step 3: Check KYC Details

Ensure that your Know Your Customer (KYC) details, such as Aadhaar, PAN, and bank account details, are linked and verified with your UAN. The KYC verification is essential to facilitate a smooth withdrawal process.

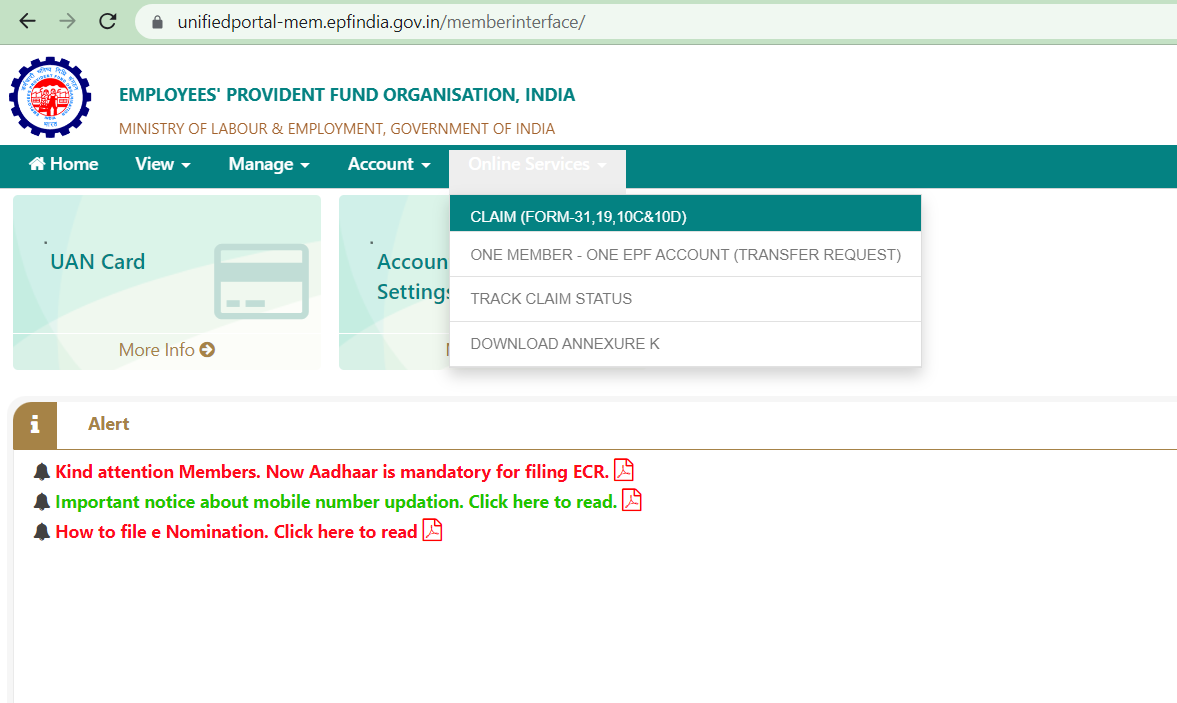

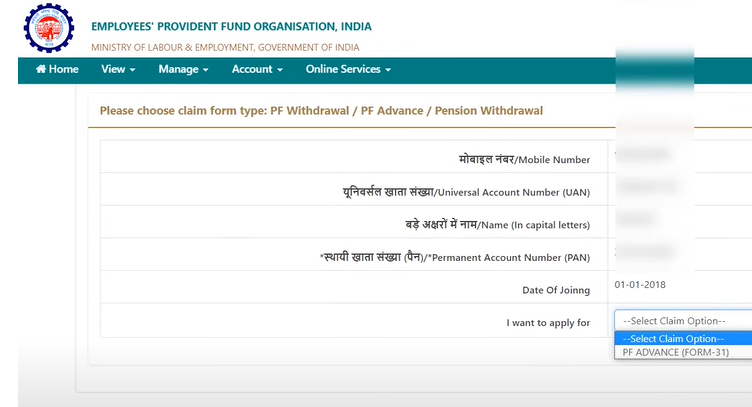

Step 4: Access Online Services

Once you are logged in, navigate to the ‘Online Services’ section and select ‘Claim (Form-31, 19 & 10C)’ from the drop-down menu.

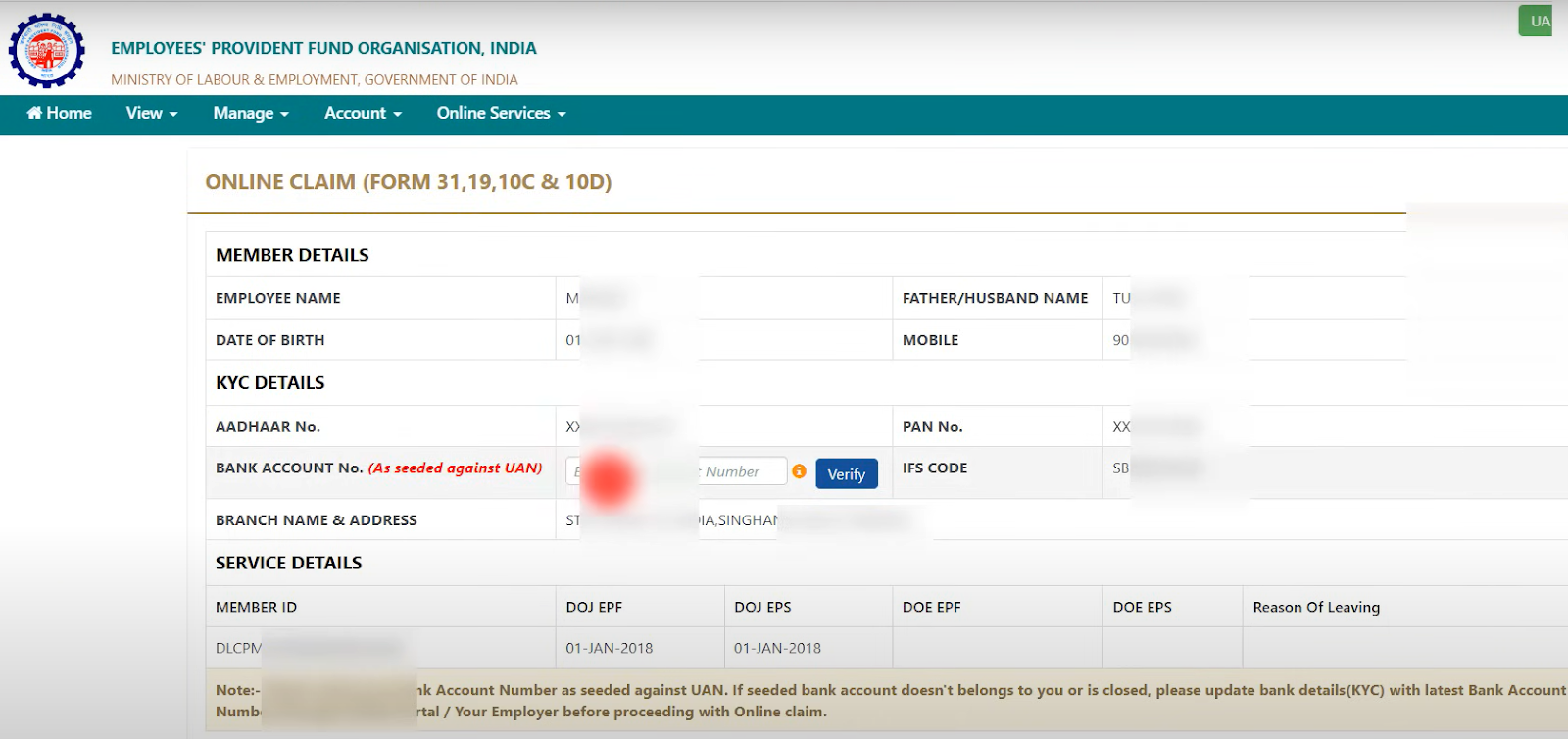

Step 5: Verify Member Details

The portal will display your member details, such as name, date of birth, and Aadhaar number. Verify the information to ensure its accuracy.

Step 6: Enter Bank Account Details

Provide your bank account details where you want the withdrawn amount to be credited. Ensure that the bank account details match the KYC details linked to your UAN.

Step 7: Certify the Application

Read the declaration carefully and certify the application to confirm that the provided information is correct and accurate.

Step 8: Select Type of Withdrawal

Choose the type of withdrawal you want to initiate. You can opt for partial withdrawal or full withdrawal, depending on the purpose (e.g., marriage, medical emergency, home loan repayment, etc.).

Step 9: Submit the Claim

After completing the form, click on the ‘Proceed for Online Claim’ button to submit the claim. The claim will be forwarded to your employer for verification.

Step 10: Employer Verification

Your employer will verify the withdrawal claim online through their employer portal.

Step 11: Amount Credited to Bank Account

Once your employer verifies the claim, the EPF withdrawal amount will be credited to your registered bank account within a few working days.

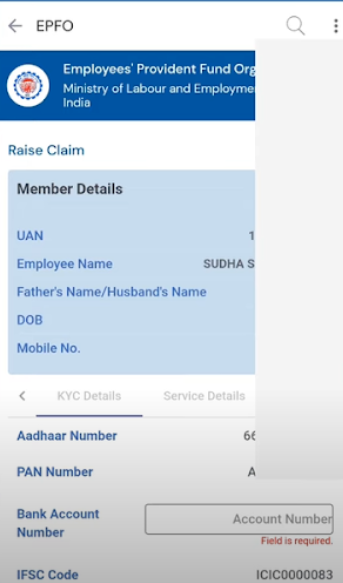

EPF Withdrawal Rules and Process (UMANG App)

The EPF withdrawal process has been digitized even further through the introduction of the UMANG app. EPFO-registered employees can apply for partial or complete EPF withdrawal online through the UMANG app as well. Below is a step-by-step guide to the EPF withdrawal through UMANG process:

-

Download and open the UMANG App on your handheld device.

-

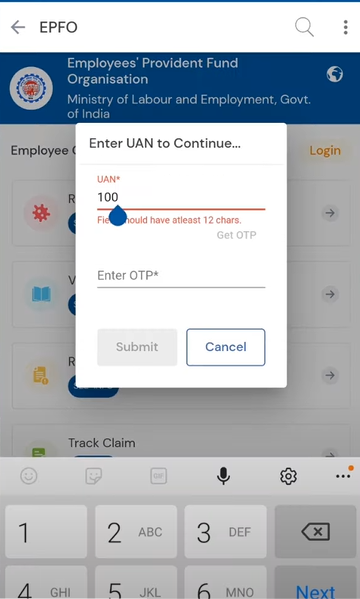

Open the app and sign into your EPFO account using your UAN number and OTP sent to your phone number.

-

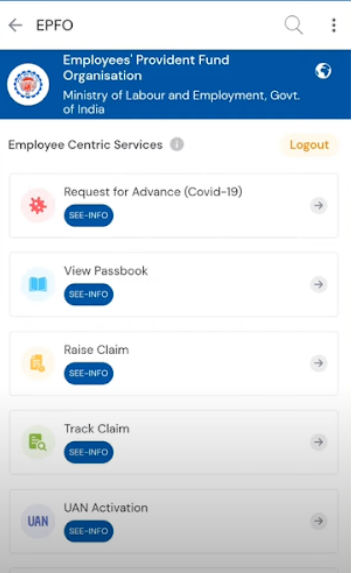

After logging in, select the ‘EPFO’ service from the list of services.

-

From the list of services provided, select the ‘Raise Claim’ option.

-

Enter the required details, like your employee bank account number, address, and other details.

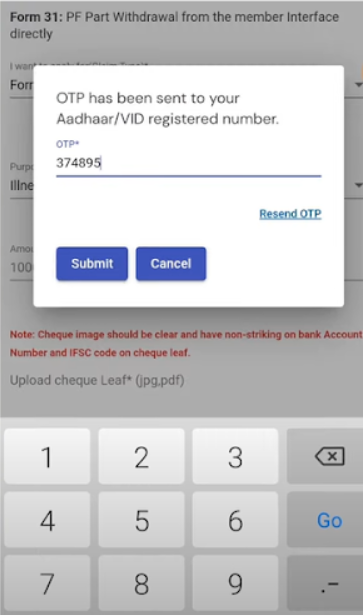

-

Select the type of withdrawal you want to make and mention other details, like the amount and purpose.

-

To submit the claim, you will have to confirm the same with an OTP.

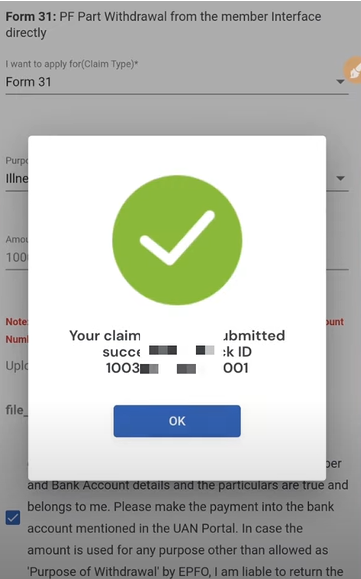

-

After you submit your claim request, you will receive a corresponding acknowledgment message and number.

Taxation on PF Withdrawal

The taxation applicable on PF withdrawal in India is subject to certain rules and conditions. The taxation of PF withdrawal depends on the duration of the PF account and the amount withdrawn. Here are the current taxation PF withdrawal rules:

-

Withdrawal before 5 years of continuous service: If an employee withdraws their PF amount before completing 5 years of continuous service, the entire withdrawn amount is taxable as per the individual’s income tax slab rate.

-

Withdrawal after 5 years of continuous service: If an employee withdraws their PF amount after completing 5 years of continuous service, the withdrawal is tax-exempt, and no tax is levied on the amount withdrawn

-

Tax Deducted at Source (TDS): If the withdrawal amount exceeds Rs. 50,000, TDS is applicable at the rate of 10% on the taxable portion of the withdrawal. However, in the 2023 Budget, the Finance Minister proposed to reduce the TDS rate from 30% to 20% for the taxable component of the EPF Scheme for non-PAN cases.

EPF Withdrawal Using Form 31 Claim Form

If you want to withdraw from your PF using a form, you can avail of Form 31 online. Fill the form and submit it at your nearest EPFO office. You can find the EPFO nearest to you using EPFO’s locator facility.

Upon submission of a duly filled form, you will receive a number and receipt for confirmation of your withdrawal request. Carefully keep the receipt till the process is completed and you receive the money in your account.

Conclusion

In summary, the EPF withdrawal rules and process are easily available on the EPFO member portal, allowing employees to access their funds for genuine needs while ensuring security and transparency. Remember to carefully review the EPF withdrawal rules and eligibility criteria and tax implications before making any withdrawal requests. If you encounter any issues or need assistance, you can reach out to the EPFO helpdesk for support.

Moreover, the taxation on PF withdrawal in India is determined by the duration of the PF account and the amount withdrawn. Note that withdrawals made before 5 years of continuous service are taxable, while withdrawals made after 5 years are tax-exempt. TDS is applicable if the withdrawal amount exceeds Rs. 50,000. It’s important for individuals to understand the taxation rules and consult with a tax professional for personalized advice.

Loan in

60 Minutes

Introduction

EPF Withdrawal Eligibility Criteria

EPF Withdrawal Rules and Process (Website)

EPF Withdrawal Rules and Process (UMANG App)

Taxation on PF Withdrawal

EPF Withdrawal Using Form 31 Claim Form

Conclusion